May

23

May

23

Tags

The Search for I-95 North

By David Nelson, CFA

By David Nelson, CFA

Markets have done their best to frustrate both Bulls and Bears in 2014. We’re halfway through the second quarter and investors are still trying to find the on-ramp to I-95 North. Detours, road blocks and a series of confusing road signs have forced many to jump from one sector to the next uncertain which path to take.

Despite mixed signals, year to date including dividends, the S&P is on track to deliver a year north of 7%. Not the fireworks from last year but respectable.

It was just last week when I talked about what I felt were canaries in the coal mine fluttering in their cages. Asset managers, which are in many ways the most representative of investor sentiment, were under performing the broad indices. Yet here we are still very close to all-time highs.

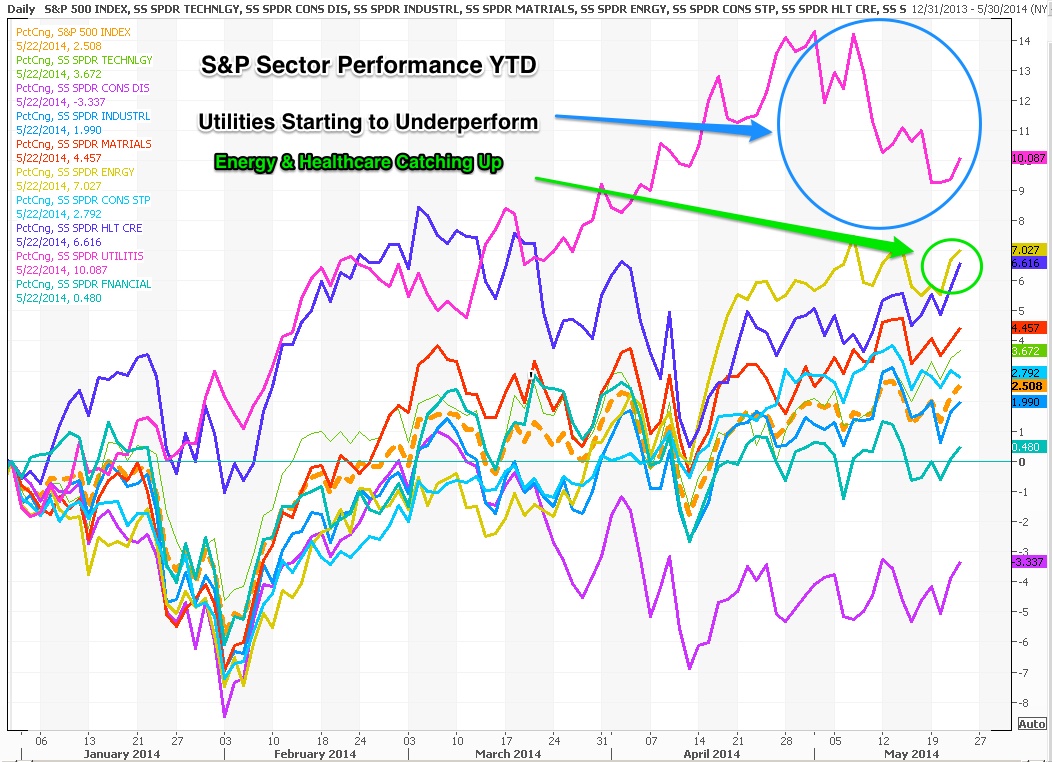

Utility Roll?

Many, including yours truly were caught off guard by the surprising strength of the Utility sector which year to date is still the best performer. My call saying the sector was an avoid on CNBC at the start of the year was clearly dead wrong. The strength of Utilities was certainly a defensive move and a precursor to falling rates.

However, as you can see in the above chart, that out-performance has started to wane. A sign of good news? Still too early to tell. It could be relieving an overbought condition but could also be signaling the bottoming of yields which sit at the lower end of a 6 month trading range. With utility valuations stretched, any move higher in yields will hit the sector hard.

Half Full or Half Empty

Prevailing wisdom at the start of the year was to be long stocks and short bonds. as interest rates were expected to climb on the back of a recovering economy. While some of the move in bonds can be explained by short covering it’s only part of the story. The strong recovery hasn’t materialized but it isn’t falling apart either. In a slow growth world investors are forced to make a choice as to whether the glass is half full or half empty.

Key for the Breakout

For markets to break out to the upside CAPEX (Capital Expenditures) has to take off. For the last few years management has picked the low hanging fruit and used excess capital to buy back stock. For the next leg of the recovery the baton has to pass to CAPEX.

Despite my squabble with many CEO’s on a range of issues, they want their stocks higher. Corporate balance sheets are in great shape and with just a little help from Washington we could see that capital put to work.

Growth vs. Value Redux

Sticking with the value call I made in March has helped drive Alpha Select returns. The under-performance of small cap vs large cap brethren is really part of the same theme. Multiples for the Russell 2000 are well above the S&P and by some measures above those we saw in the late 90’s.

Since I penned The Worm Has Turned back in March, I get a lot of questions from investors asking; “should I stay completely out of growth stocks?”

Avoiding growth isn’t the answer. What’s important is how much you’re paying for it.

Avoid the Macro – Focus on the Micro

Avoid the Macro – Focus on the Micro

As the market churns and grinds ever so slowly higher the message seems to be; “focus less on the market and spend more time honing in on individual companies. Trading around the noise isn’t helping.

Macro signals and economic data has been confusing at best sending investors on a series of detours. Looking at stocks from the bottom up focused on individual names has been a much better road map.